Introduction

Most developed countries provide universal or near-universal health insurance coverage. The US has lagged behind with 49.9 million individuals, or 16.3% of the population, reportedly uninsured as recently as 2010. Policy debates in the US, where proponents of universal coverage have argued that extending coverage to the uninsured would result in better access to health care, improved health outcomes, and ultimately lower costs, have culminated in the enactment of the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act (collectively referred to as the ACA) in 2010. In tandem with the policy debate, health economists have explored the impact of health insurance on health outcomes using empirical methods. Nevertheless, the evidence so far remains inconclusive. Both those favoring universal coverage and those arguing for limited steps were able to find some support for their respective positions, albeit on a selective basis. Although supporters of the legislation claim that the phased implementation of the ACA will dramatically reduce the ranks of the uninsured, millions of Americans are expected to remain without any coverage. Gaining a better understanding of what the health economics literature offers to this policy discussion thus remains highly relevant.

Economic theory suggests that health insurance can serve a dual purpose of protecting people against the financial burden of illness and of increasing access to care to meet unmet health care needs. Conventional expected utility theory, which is widely applied to evaluate the demand of health insurance, considers any medical expenditure to be a loss of income. In view of this theory, the purchase of health insurance or medical care reduces a consumer’s wealth. For the research question at hand that investigates whether health insurance improves health, medical expenditures may instead be considered an input in the health production function (Grossman model). Accordingly, the stock of health can be improved by investments in medical care which the purchase of insurance enables. Most of the relevant literature assumes such a model, at least implicitly. At the same time, the benefits of health insurance coverage may be partially offset by the effects of exante moral hazard (Moral Hazard is the change in behavior that occurs as a result of becoming insured. Ex-ante moral refers to the change in the probability of illness or injury. Expost moral hazard refers to the size of the loss (medical expenditures) after the illness/injury occurred.). Accordingly, people with health insurance coverage may have less financial incentives to engage in healthy behaviors that prevent injury and illness.

A body of existing research supports a negative association between the lack of health insurance and access to care, and in turn, a positive association between access to care and health outcomes. Descriptive studies report that in the US the uninsured have less access to health care, higher risks of unmet health needs, and poorer health outcomes. For example, research has shown that uninsured adults use 60% less ambulatory health services and 30% less inpatient health services than insured adults. In addition, the uninsured are more likely to delay seeking care, to report not being able to see a physician due to costs, and to require costly emergency care. Even among patients that did see a clinician, only 18% of uninsured patients received all recommended follow-up treatment in comparison to 30% of insured patients. In comparison to insured adults, the uninsured are also more likely to have a lower self-reported health status and are more likely to be diagnosed at an advanced stage of cancer, suffer from cardiovascular diseases, exhibit worse glycemic control, and experience higher in-hospital mortality rates.

Although the positive association between health insurance coverage and health outcomes appears to be convincing, the issue has been a matter of considerable controversy among empirical economists. Mere associations may mask the fact that healthier individuals tend to be better equipped to obtain health insurance, leading one to overstate the actual contribution of insurance to health, a problem related to reverse causality and simultaneity in econometric estimation. To address this general concern different methodological approaches have been undertaken, perhaps contributing to occasionally conflicting results. In addition, this literature encounters measurement issues which merit further scrutiny.

In this article, the aim is to shed light on the nuances in the literature on the causal effect of health insurance on health outcomes. The objective here is to clarify the limitations of this literature and to provide a deeper understanding of the causal pathways between insurance and health, ultimately to better inform the policy debate. As will be seen, certain patterns have emerged: Lack of insurance may be more of an adverse factor for mortality and generic health outcomes although its effects on condition-specific measures are more complex. In addition, interruptions in insurance coverage can be just as harmful as the complete lack of insurance. This review focuses primarily on the US, and its private segment of the market, where the acquisition of insurance has largely been a matter of individual choice, at least before the implementation of ACA. However, inferences are also drawn from the literature on government sponsored insurance, namely, Medicare and Medicaid, where insurance coverage is simply assigned to individuals based on age and income, and the state in which the individual resides.

The remainder of this article is divided into five sections. First, there is a brief description of the characteristics of the US uninsured population and the anticipated changes for health insurance coverage under the ACA. Second, the methodological challenges related to estimating the impact of insurance on health are discussed. Third, the methods used in the source literature are illustrated. Fourth, general findings in the source literature are presented. Finally, challenges for future research are discussed and emerging implications of the ACA comes in as conclusion.

The Uninsured And The US Health Care System

In the US, historically, the elderly and the disabled have received public insurance coverage through Medicare, whereas the poor received public insurance through Medicaid. Otherwise, health insurance coverage has effectively been tied to employment with 90% of all privately insured individuals receiving their coverage through their employers. Roughly 50% of employees participate in employer-sponsored health insurance coverage and consequently a large portion of employees, especially temporary and part-time employees, lack insurance. Not surprisingly, the contraction in the labor market that accompanied the Great Recession in the early twenty-first century also contributed to the rising number of the uninsured. Between 2008 and 2010, nearly one-quarter of working-age adults reported that they or their spouse had lost their job and more than 50% of these people became uninsured. Historically, a significant portion of the uninsured population consisted of relatively vulnerable groups such as the near poor and near elderly. Individuals belonging to these groups are more likely to experience unemployment compared with higher income or young people, and are also more likely to suffer from adverse health events. Yet, income and age restrictions precluded these individuals from enrolling in public insurance programs such as Medicaid or Medicare, leaving them at a higher risk of remaining uninsured.

The ACA is expected to greatly reduce the number of uninsured. Under the ACA, most US citizens and legal residents will be required to have health insurance, a number of states will expand Medicaid to include the nonelderly population at 133% of the federal poverty line, and states are engaging in setting up health insurance ‘exchanges’ offering plan choices to previously underserved individuals. In addition, federal subsidies will be made available to small firms and individuals for the purchase of insurance. Nevertheless, the ACA will only reduce the number of uninsured by half. The Congressional Budget Office estimated that by 2019, 23 million Americans will remain uninsured even if the ACA is fully and successfully implemented. The small penalties levied against those opting out of the system, the so-called ‘mandates,’ may not be sufficient to outweigh the incentives not to join. Moreover, certain population groups are exempted.

Methodological Challenges

In this section, methodological challenges facing research estimating the causal effect of insurance on health are discussed, starting with identifying the uninsured, defining health outcomes, and addressing endogeneity bias.

Identifying The Insured And Uninsured

Identifying the uninsured is a difficult task. In most household surveys, individuals tend to misclassify themselves as being insured or uninsured due to the way health coverage is defined. Misclassification occurs mainly around changes in employment status, due to confusion about receiving coverage through another family member, or simply because of poor recall when survey questions require longer retrospective periods. Another type of misclassification occurs when Medicaid enrollees or beneficiaries of other public programs do not recognize these programs to be a form of health insurance, leading some to erroneously identify themselves as uninsured. Indeed, comparisons of survey data with administrative data have demonstrated that surveys consistently underestimate insurance coverage. Underreporting of insurance coverage has been proven to be a particular problem for Medicaid with specific evidence of underreporting available for all Medicaid beneficiaries in California and Maryland, and nationwide for child beneficiaries. As a result, the estimated prevalence of uninsurance varies somewhat between surveys. For instance, a comparison of the Health Retirement Survey (HRS) and the Medical Expenditure Panel Survey (MEPS) in 2006 yielded an uninsurance rate of 10% and 12%, respectively.

Another form of measurement error occurs when continuity of coverage is of interest. The majority of studies reviewed used insurance coverage at the time of interview as the key explanatory variable. However, in the US, particularly in the private sector, people frequently gain and lose health insurance coverage, a phenomenon also known as churning. Between 1998 and 2002, churning affected 22% of the population. Much like the complete absence of insurance, churning may adversely affect health due to discontinuity of care and delays in treatment. Among children and adults, loss of insurance is associated with a lower likelihood of having a primary care provider, getting check-ups, or receiving the recommended follow-up care. Intermittent health insurance coverage may thus affect health outcomes in a similar fashion as the lack of health insurance coverage. A number of nationally representative surveys including the HRS, the MEPS, and the National Health and Nutrition Examination Survey (NHANES) ask respondents to report their health insurance status retrospectively for a 3–18month period. Several studies made use of this feature to define insurance in terms of frequency of changes or to draw comparisons between the continuously insured, the intermittently insured, and those lacking insurance coverage over a fixed period.

Although this article focuses only on the provision of insurance, note that health insurance is heterogeneous and variations in generosity of health insurance benefits can occur not only between general insurance categories such as Medicaid, Medicare, and private, but also within such groupings. The lack of information about insurance generosity in household surveys creates a major practical limitation for related research. The literature reviewed here is generally silent on this issue.

Measuring Health Outcomes

The source literature assessed the impact of health insurance on three broad categories of health outcomes: mortality, condition-specific morbidity, and generic health measures. The majority of studies relied on mortality-based measures, such as all-cause mortality, disease-specific mortality, or survival rates. Condition-specific morbidity measures pertain to the clinical status of a given illness or medical condition. Examples from the literature include low birth weight, obesity, and cancer disease stage.

The term ‘generic health measures’ is used to describe aspects of functioning in health related daily activities which are not necessarily disease specific. Generic health measures can be either unidimensional or multidimensional. Unidimensional measures include self-reported health indicators, such as one’s overall ranking or the number of chronic conditions. Multidimensional measures combine several subjective indicators of physical and mental health into a single additive scale.

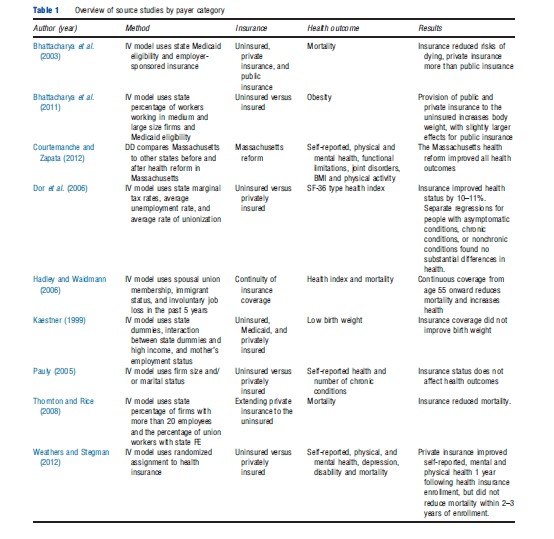

Expert research in the psychosocial literature has validated the use of self-reported health rankings. In addition, the health services research literature offers well developed and validated methodologies to construct multidimensional health indices, such as the Short Form-36 (SF-36). Data elements that comprise these indices are now routinely included in nationally representative surveys such as the National Health Interview Survey and the HRS. For example, Dor et al. (2006) and McWilliams et al. (2007) combined self-reported general health, the number of physical limitations, and pain into a modified SF-36 health index. Table 1 provides a brief description of the literature used in this article. Although this article focuses primarily on private insurance a summary of the evidence on the causal effect of Medicaid and Medicare is available in Table 1.

Although each of the above health outcome categories offers certain advantages, they are also affected by certain measurement issues and interpretation problems. An obvious advantage of using mortality as a summary measure of adverse outcomes is that death is completely unambiguous, and it is easily verifiable in most data systems. Thus, mortality is susceptible to minimal measurement error. However, although mortality reflects the lowest boundary of health, it does not capture the path of declining health over the individual’s life cycle. In contrast, condition-specific measures may capture the stage and severity of illness, but targeting a narrowly defined condition may lead researchers to overlook other important dimensions of health. Moreover, most surveys rely on self-reporting of morbidity indicators, and thus require respondents to possess specific and time sensitive knowledge of their own disease.

Generic health measures provide a broader view of health that transcends any single condition. Because general health measures are based on a person’s functioning, they can be used for more general population groupings than the above. Another advantage is that most household surveys provide validation of respondents’ replies to questionnaires. However, by trading off specificity generic measures may mask insurance ‘treatment’ effects that might apply to certain conditions but not others. Further adding to measurement error, interpretations of good functioning may vary by respondents’ age, gender, and other groupings. However, the health services literature suggests that combining several unrelated aspects of health helps mitigate reporting error in multidimensional indices. Finally, generic health measures may reflect health status changes, with a time-lag, rather than responding instantaneously.

In summary, both insurance coverage and health status indicators, excluding mortality, are subject to measurement error. In regression analysis measurement error in the dependent variable (health status) increases standard errors but does not produce a biased estimator. However, measurement error in the explanatory variable (insurance) biases the coefficient estimates, although the direction of the bias is predictable (toward zero) as long as measurement error does not appear in any other independent variables in the model.

Endogeneity Of Insurance In Health

Selection, reverse causality, and omitted variable bias pose other methodological challenges. Each one of these issues presents a special case of endogeneity, whereby ordinary least square estimates of the effect of insurance on health may be biased due to a correlation between a regressor and the regression residual. A myriad of institutional and behavioral processes underlie endogeneity, making it difficult to ascertain whether the bias occurs in an upward or downward direction.

The private insurance market is affected by selection problems, which arise when there is information asymmetry between insurers and insured. Adverse selection occurs when insurance companies attract sick people who are more likely to need and use health care, and when healthy people, who do not anticipate incurring high medical expenses, choose cheaper but less generous plans or opt out of insurance altogether. Adverse selection would bias the estimated relationship between insurance and health downwards. Auspicious selection occurs when insurers try to attract the good risks (e.g., healthy or young individuals), while making plans unattractive for bad risks (e.g., those with preexisting conditions). Auspicious selection would bias the estimated relationship upwards. Both adverse and auspicious selection, and related estimation biases, will be even worse when insurance risks are experienced rated (as in the individual insurance markets) rather than community rated (group insurance).

Reverse causality occurs when health affects health insurance status. The direction of this bias is also unknown. People in poor health are more likely to buy health insurance (or purchase more generous coverage) than healthy people, as they anticipate a greater need for care. Conversely, in the mostly employer-based private segment of the US market, poor health tends to be associated with job loss and hence loss of insurance, particularly in periods of high unemployment.

Finally, a type of omitted variable bias occurs when the individual’s insurance choice is determined by some traits that also affect health but are unobservable to the researcher. For example, risk-averse individuals are more likely to hedge the risk of income loss by purchasing insurance, although simultaneously displaying risk-avoiding health behaviors. Similarly, certain people are better equipped to asses both insurance and health care information and act preventively, an unobservable trait sometimes referred to as health ability. Reliable measures of risk aversion, health ability, and underlying health behavior are rarely available in observational datasets. Consequently, in classic regression analysis included explanatory variables may be correlated with the error term.

Estimation Methods

Three different approaches to measuring the causal effect of insurance on health as they appear in the literature is discussed: Studies using instrumental variable (IV) techniques, studies using quasi-experimental designs, and randomized experiments. (Quasi-experiments encompass both the natural experiments and IV studies that are discussed. For the purpose of this article, natural experiments and IV approaches are discussed separately because natural experiments rely on exogenous source of variation in the treatment assignment, whereas the IV approach uses a continuous probability distribution of the treatment assignment.) In the context of private markets, most studies used IV approaches to address the endogeneity issue previously discussed, allowing for probability distributions of the insurance choices made by individuals. In the context of government programs where insurance coverage is simply assigned to individuals based on an arbitrary (exogenous) criterion, quasi-experimental techniques are more relevant. Although the primary interest is in the private segment of the market, some attention is devoted to quasi-experimental evaluations of Medicare and Medicaid in order to draw inferences for future research directions given the recent enactment of private mandates in the US. Finally, the very limited but important literature on controlled experiments that allow for random assignment of individuals into insured and uninsured states is discussed.

Instrumental Variable Estimation

The issue of endogeneity can be addressed by simultaneous estimation of insurance choice and a health outcome using IVs. Briefly, IVs would be included in the insurance equation but excluded from the health equation based on the following criteria: First, the instrument must be uncorrelated with the error in the health equation. As this is not easily verified, researchers’ choice of IVs must rely on economic theory and solid reasoning when choosing appropriate instruments. Second, the instrument must be strongly correlated with insurance choice (the latter can easily be tested).

A variety of instruments have been used, but their validity has been repeatedly called into question. Examples include state-level variables, firm-level variables, certain individual level variables, or some combination of all of the above (source studies and their instruments are described in Table 1). A number of studies employed indirect tests that provide a modicum of confidence. For instance, arguing that state-level Medicaid eligibility and average firm size are independent of health (mortality) but affect the ease with which people obtain Medicaid or employer-sponsored insurance, Bhattacharya et al. (2003) examine their strength and relevance as instruments when estimating the effects of public and private insurance on health among human immunodeficiency virus (HIV) patients, using data from the HIV Costs and Services Utilization Study. The authors report a strong correlation between their instruments and insurance coverage based on statistical tests (e.g., the Wald statistic), and a high degree of relevance, based on a reasonable falsification test. (The instruments would be irrelevant if they were to predict health outcomes for an unrelated population. Using a sample of Medicare beneficiaries as an alternative to the original sample of HIV patients, Bhattacharya et al. show this is not the case, suggesting that their instruments are valid.)

In a related example, Dor et al. (2006) used state marginal tax rates, average unemployment rate, and average unionization rates to instrument insurance. The study population included adults age 45–64 from the 1992 to 1996 HRS surveys. Substantial literature suggests that state-level tax burden is uncorrelated with health but to be positively correlated with insurance participation. Similarly, union membership is positively correlated with being offered insurance coverage, whereas unemployment is negatively correlated with private health insurance coverage. However, the use of marginal tax rates in the first stage results were only weakly correlated with health insurance. Some critics raised questions about the validity of unemployment as an instrument, arguing that macroeconomic downturns may affect health not only through insurance loss but also because they affect health behaviors such as drinking and exercise. It should be noted, however, that previous versions of the study used county-level firm sizes as an instrument, yielding essentially the same results for the effect of insurance on health (Dor et al., 2003).

Various combinations of person-level variables have also been used to instrument insurance. Among these are employer size, marital status, spousal union membership, immigrant status, involuntary job loss, and self-employment status (Table 1). Again, the validity of any of these variables can be questioned, given that is unlikely that they do not affect health in some indirect way. For instance, for some people job loss may lead to depression or loss of physical activity, leading to deterioration in overall health; foreign-born workers from poor countries may have worse health status than native-born US workers, suggesting that immigration status is and negatively correlated with health. Spousal union membership may be the most appealing variable in terms of avoiding systematic correlation between the instrument and the subject’s health. However, any study to date that has attempted to test the validity of this instrument by itself is unheard of.

Quasi-Experiments

Quasi-experimental methods including difference-in-difference (DD) models and Regression Discontinuity Design (RDD) models have been used to get around the difficulties of modeling endogeneity and selecting appropriate IVs. These models, which borrow from the more general program evaluation literature, rely on finding cases where insurance can be treated as an exogenous intervention. In DD models, a treatment group and a comparison group are identified and the impact of the treatment is inferred from the difference between the changes experienced by the two groups over time; DD models have been widely used to evaluate Medicaid expansions and outcomes in US states, whereas RDD models are more readily applied to evaluations of Medicare (Table 1). In an innovative study, Polsky et al. (2009) employ DD to Medicare by comparing health status for the previously uninsured and continuously insured before and after enrollment at age 65.

RDD models exploit exogenous policy rules, yielding a comparison of individuals above and below a fixed cutoff point. A critical assumption for RDD models is that by tracking individuals closely around the cut off trends unrelated to the policy are essentially filtered out. RDD models are commonly used to evaluate Medicare because of its generally arbitrary eligibility criterion which assigns individuals to the program at age 65. For example, using the 1991–2002 Behavioral Risk Factor Surveillance System, Decker (2005) estimated the effect of Medicare eligibility on breast cancer stage and survival. To ensure that other age-related changes such as retirement were not erroneously captured in her eligibility indicator, Decker also controlled for employment status; although this additional variable was statistically significant in her model, it did not alter the estimated Medicare effect. In a variant of RDD, McWilliams et al. (2007) used a linear spline regression to compare health outcomes for people before and after acquiring Medicare.

Randomized Controlled Experiments

Given the difficulty posed by endogeneity and concerns over nonsymmetry between treated and controls in quasi-experimental studies, ideally, the impact of insurance on health would be inferred from randomized controlled trials (RCT) whereby people are randomly assigned to separate categories of those receiving health care coverage and those without any insurance. However, RCTs are virtually impossible to implement due to both practical and ethical reasons. Nevertheless, two recent policy experiments offer close approximations; the first was carried out by the US Social Security Administration (SSA), and the second was implemented by the state of Oregon.

Focusing on Social Security Disability Insurance (SSDI) beneficiaries, the SSA experiment was designed to test whether making medical benefits available to these beneficiaries immediately, rather than requiring a mandatory 2 year waiting period improves health outcomes. Accordingly, between October 2007 and November 2008, a subset of newly enrolled SSDI beneficiaries was asked to participate in the Accelerated Benefits (AB) demonstration. Those that agreed to participate were randomly assigned to groups receiving a relatively generous health insurance plan versus remaining uninsured for 2 more years. The AB demonstration thus provided a unique opportunity to test whether having insurance improves short-term health outcomes (Weathers and Stegman, 2012).

In 2008, Oregon had enough funding to expand enrollment to 10 000 low-income adults. Later dubbed the Oregon health insurance experiment (Oregon HIE), beneficiaries were randomly chosen by lottery from the pool of eligible candidates, thereby creating two groups of covered and noncovered individuals. The origins of the Oregon HIE can be traced to the RAND Corporation Health Insurance Experiment of the late 1970s. However, the RAND Corporation study focused on cost sharing levels with insurance rather than outright withdrawal of insurance.

Analysis of the first year’s results offers valuable insights, but also highlights limitations of RCTs and their approximations (Finkelstein et al. 2011). At the end of the year, insurance coverage appeared to improve participants’ self-reported physical and mental health in comparison to the uninsured control group. However, when the timing of these improvements was examined more carefully, the researchers found that they occurred before the actual initiation of health care. This may suggest a type of placebo effect whereby the mere availability of health insurance provides the individuals with a sense of wellbeing and a heightened perception of health status.

Results: Health Insurance Effects By Type Of Health Measure And Study Population

Having noted methods, studies can be further classified by type of health outcome measure and type of population studied. Results are summarized accordingly:

Health Outcomes

Overall, the large majority of studies agree that health insurance coverage reduces the risk of mortality. For example, using state-level panel data from 1990 to 2000 and firm size and union membership to instrument insurance, Thornton and Rice (2008) concluded that extending private insurance to the uninsured would reduce adult mortality and save more than 75 000 lives annually. Similarly, using union membership, immigrant status, and involuntary job loss as instruments for insurance, Hadley and Waidmann (2006) concluded that extending insurance coverage to all Americans between the ages of 55 and 64 would reduce mortality in this age group. Furthermore, Bhattacharya et al. (2003), using the 1996–1998 HIV Cost and Services Utilization Study, concluded that HIV patients with private health insurance coverage had a 79% lower relative risk of dying than HIV patients without insurance. And, HIV patients with public health insurance had a 66% lower relative risk of mortality than HIV patients without insurance. Weathers and Stegman (2012) is the only study to find no effect of insurance coverage on mortality; their brief follow-up of 3 years did not allow for identification of longer term effects in their experimental data.

Similarly, a majority of studies found positive effects of health insurance on generic health measures. Weathers II and Stegman found that insurance improved self-reported mental and physical health of SSDI beneficiaries one year after receiving health insurance. Using the 1992–1996 HRS, both Dor et al. (2006) and Hadley and Waidmann (2006) found that insurance improved health as proxied by SF-36 type health indices. Similarly, Courtemanche and Zapata (2012) concluded that the Massachusetts health care reform legislation improved a number of health outcomes, including self-reported general health, physical limitations, and a health index. An exception can be found; Pauly (2005) found no significant effect on self-reported general health or the number of adult chronic conditions using the 1996 MEPS.

In contrast, insurance effects vary across condition-specific measures. Private insurance did not reduce the share of infants with low birth weights (Kaestner, 1999) and coverage did not benefit people with chronic conditions more than people without (Dor et al., 2006) while initiation of Medicare coverage improved outcomes for women with breast cancer. In one interesting case, private insurance coverage actually increased obesity prevalence (Bhattacharya et al. 2011). One way to reconcile seemingly contradictory results would be to assume that ex-ante moral hazard (in this case more eating, less physical activity and the like) affects some conditions more than others and that the adoption of risky behaviors offsets the health benefits of insurance unequally. The association between health insurance and health behaviors was not explicitly treated in the literature surveyed in this article. Although informative, these findings may not necessarily generalize to other settings given that the efficacy of medical treatment, which insurance enables, is not the same for all medical conditions and diagnoses.

Reconciling Competing Health Measures

Using the setting of transitions into Medicare, an important discussion on the relationship between mortality and generic health measures took place through two interrelated studies (McWilliams et al., 2007; Polsky et al., 2009). In much of the previous literature summarized in Table 1, condition-specific outcomes, and generic health measures were treated as mutually exclusive outcomes. A point of agreement in both of these studies is the need to account for censoring due to mortality even when other health outcomes are of interest, particularly when longitudinal data are employed. Indeed, the two studies using essentially the same database report that attrition due to mortality was responsible for a 15% reduction in sample size during a 13-year period for a population of people around Medicare eligibility. However, although Polsky et al. and McWilliams et al. agreed on the problem, they disagreed on the methods needed to address it, leading them to engage in a lively debate in subsequent articles.

Although both studies used similar quasi-experimental designs (DD and RDD, respectively, see Section Estimation Methods) and share some findings, their results differ for some outcome measures; the differences have been attributed to the way the authors deal with mortality-related censoring. Both studies compared previously uninsured to insured before and after entering Medicare, and both studies drew the same years and health outcomes from longitudinal HRS data (Table 1). Both studies found no significant effect on self-reported health status, mobility, and pain, but differed in their findings for agility and symptoms of depression. In addition, the effect of health insurance was significant for an index of health outcomes only in the McWilliams study. To attenuate sample attrition, McWilliams et al. used an inverse probability weighting technique to assign higher weights to individuals who had died on the basis of antecedent health trends, insurance coverage before age 65, and demographic and socioeconomic characteristics. However, this approach may not be accurate given that death is not a random event. To address the nonrandomness issue Polsky et al. used a novel approach simulating the predicted probability of health state transitions, with death as one of the included health states. Interestingly, when Polsky et al. incorporated inverse probability weighting into their original DD design they found similar results as McWilliams et al. This suggests that disparate results were caused by the different ways of accounting for mortality, rather than choice of general technique. The discussion underscores the need for researchers to continue to design innovative and more complete measures of health outcomes.

Vulnerable And Special Populations

The health effects of insurance vary for populations stratified by medical conditions or vulnerability, with vulnerable people benefiting more from health insurance than others. For example, although the RAND Corporation experiment did not find an effect of insurance generosity on the health status of the average adult, insurance generosity did have a positive effect on health for individuals with high blood pressure (Keeler et al., 1985). Similarly, private insurance positively affected the health of HIV patients (Bhattacharya et al., 2003), Medicaid health benefits were larger when provided at early childhood than at later childhood (Currie et al., 2008), and adult patients nearing the Medicare enrollment age with cardiovascular disease or diabetes benefited more from insurance coverage compared with their counterparts with any health condition (McWilliams et al., 2007). More generally, Weathers and Stegman (2012) attributed the larger effect of health insurance in the AB demonstration as compared with the Oregon lottery to the relatively poorer health and disability status of persons in the former cases. Further research is needed to identify which patient populations would benefit most from insurance coverage.

Continuity Of Coverage: Effect Of Churning

A few studies sought to go beyond the simple insured/uninsured dichotomy and evaluated the effects of discontinuities in insurance coverage over time (churning). These begin with a comparative, but mostly descriptive study, (Baker et al. 2001), followed by a more rigorous study by Hadley and Waidmann (2006); both studies found that adults who were continuously insured had better health outcomes, as measured by summary health scores, compared to those with intermittent private insurance. Hadley and Waidmann (2006) followed preretirement age adults up to eight years before reaching the Medicare eligibility age of 65, and analyzed the impact of health insurance on health status at that point. Insurance coverage was defined as percentage of time a person has insurance over the observation period before age 65. Although this created certain lumpiness in their insurance measure (the Health and Retirement Study, from which they draw their data, is a biannual survey thus requiring the assumption that people remain in the same insurance category in between survey years) it allowed the authors to estimate effects of continuous insurance versus intermittent insurance. They used similar IVs as those described in Section Estimation Methods to purge their insurance variables from endogeneity bias. McWilliams et al. (2007) also report that continuous insurance coverage appears preferable to intermittent coverage for a host of health outcomes. Despite progress made in modeling the dynamic impacts of insurance on health, there appears to be a need for additional research on the intertemporal effects of insurance.

Conclusion

This article highlights the myriad of methods used to estimate the impact of health insurance on health and their limitations. Despite the wide variation in research designs and methods applied, and in particular, the difficulty of identifying valid instruments, a number of common themes can be found. First, it appears that insurance coverage impacts mortality and generic health outcomes more significantly than most condition-specific outcomes, at least in the studies reviewed. Second, certain vulnerable populations such as infants, the disabled, and HIV/acquired immune deficiency syndrome patients appear to benefit from insurance more than the general population. Third, despite the availability of a yet small and largely descriptive body of research on the intertemporal dynamics of insurance, there is compelling evidence to suggest that continuity of health insurance coverage is particularly effective in maintaining health, and that having sporadic coverage offers little protection over little protection over having no coverage at all.

Relevance For Health Reform

With the advent of health care reform, the US appears to be moving closer to universal coverage, albeit not fully. The full effect of reforms, in terms of reducing the ranks of the uninsured, remains to be seen. A major hurdle in the implementation of the reforms was crossed when the Supreme Court’s ruling of June 2012 largely upheld the constitutionality of two major provisions of the ACA: First, the individual mandate and second, the Medicaid expansion (expanding Medicaid eligibility to almost all people under age 65 with incomes at or below 138% of the Federal Poverty Line). The individual mandate requires most people to maintain a minimum level of health insurance coverage starting in 2014; however, the ACA contains several exemptions to the mandate, which allow several millions of Americans to remain uninsured by choice. Moreover, the court’s ruling made Medicaid expansion in the ACA optional for the states, and despite the availability of generous federal matching funds, some states have opted not to expand their Medicaid programs. The next hurdle in the path of health care reform and the ACA in terms of moving closer to universal coverage is the design and implementation of state insurance marketplaces (exchanges) that are meant to pool and subsidize employees of small of firms and the self-insured. These marketplaces are intended to be fully functional by early 2014. However, delays are anticipated in many states and participation rates remain to be seen.

Thus, in all likelihood, the debate regarding the value of extending coverage to the uninsured will continue to rage even after the implementation of the ACA. From a methodological perspective, studies on the relationship between insurance availability and health outcomes in the private segment of the US market were hampered by statistical identification issue, making it difficult to ascertain the precise contribution of coverage to health. The anticipated broad expansions of insurance coverage in the US should provide future researchers, opportunities to conduct quasi-experimental studies of private expansions, much like has been done previously in the context of Medicaid and Medicare. It is noted that the debate over this issue is not limited to the effects on health. Other important arguments for providing insurance include efficient use of resources, cost containment, equal access to care, and social protection.

Bibliography:

- Baker, D. W., Sudano, J. J., Albert, J. M., Borawski, E. A. and Dor, A. (2001). Lack of health insurance and decline in overall health in late middle age. New England Journal of Medicine 345(15), 1106–1112.

- Bhattacharya, J., Bundorf, K. M., Pace, N. and Sood, N. (2011). Does health insurance make you fat? In Grossman, M. and Mocan, N. (eds.) Economic aspects of obesity, 1st ed., pp 35–64. Chicago, IL: National Bureau of Economic Research.

- Bhattacharya, J., Goldman, D. and Sood, N. (2003). The link between public and private health insurance and HIV-related mortality. Journal of Health Economics 22(6), 1105–1122.

- Courtemanche, C. J. and Zapata, D. (2012). Does universal coverage improve health? The Massachusetts experience, pp 1–52. NBER Working Paper Series 17893. Cambridge, MA: National Bureau of Economic Research.

- Currie, J., Decker, S. and Lin, W. (2008). Has public health insurance for older children reduced disparities in access to care and health outcomes? Journal of Health Economics 27(6), 1567–1581.

- Decker, S. L. (2005). Medicare and the health of women with breast cancer. The Journal of Human Resources 40(4), 948–968.

- Dor, A., Sudano, J. J. and Baker, D. W. (2003). The effect of private insurance on measures of health: Evidence from the Health and Retirement Study, pp 1–42. NBER Working Paper Series 9774. Cambridge, MA: National Bureau of Economic Research.

- Dor, A., Sudano, J. and Baker, D. W. (2006). The effect of private insurance on the health of older, working age adults: Evidence from the Health and Retirement Study. Health Services Research 41(3), 975–987.

- Finkelstein, A., Taubman, S., Wright, B., et al. (2011). The Oregon health insurance experiment: Evidence from the first year. NBER Working Paper 17190 Cambridge, MA: National Bureau of Economic Research.

- Hadley, J. and Waidmann, T. (2006). Health insurance and health at age 65: Implications for medical care spending on new Medicare beneficiaries. Health Services Research 41(2), 429–451.

- Kaestner, R. (1999). Health insurance, the quantity and quality of prenatal care, and infant health. Inquiry 36(2), 162–175.

- Keeler, E. B., Brook, R. H., Goldberg, G. A., Kamberg, C. J. and Newhouse, J. P. (1985). How free care reduced hypertension in the health insurance experiment. JAMA: The Journal of the American Medical Association 254(14), 1926–1931.

- McWilliams, J. M., Meara, E., Zaslavsky, A. M. and Ayanian, J. Z. (2007). Health of previously uninsured adults after acquiring Medicare coverage. JAMA 298(24), 2886–2894.

- Pauly, M. V. (2005). Effects of insurance coverage on use of care and health outcomes for nonpoor young women. The American Economic Review 95(2), 219–223.

- Polsky, D., Doshi, J. A., Escarce, J., et al. (2009). The health effects of Medicare for the near-elderly uninsured. Health Services Research 44(3), 926–945.

- Thornton, J. A. and Rice, J. L. (2008). Does extending health insurance coverage to the uninsured improve population health? Applied Health Economics and Health Policy 6(4), 217–230.

- Weathers, R. R. and Stegman, M. (2012). The effect of expanding access to health insurance on the health and mortality of Social Security Disability Insurance beneficiaries. Journal of Health Economics 31(6), 863–875.

- Decker, S. L. and Rapaport, C. (2002). Medicare and inequalities in health outcomes: The case of breast cancer. Contemporary Economic Policy 20(1), 1–11.

- Sudano, J. J. and Baker, D. W. (2006). Explaining US racial/ethnic disparities in health declines and mortality in late middle age: The roles of socioeconomic status, health behaviors, and health insurance. Social Science and Medicine 62(4), 909–922.