Introduction

The primary benefit from health insurance for risk averse people is to spread the risk of high expenses. But it can also affect the use of medical care. Although insurance coverage can then do harm to efficiency by distorting consumer/patient demand for medical services, it can also provide potential benefit by offsetting existing distortions. An important further consideration in some countries and in some settings, however, is whether such corrections will be offered by competitive insurers and accepted by buyers in voluntary insurance markets. Will market insurance coverage, that nudges people to do the right thing, be supplied and purchased?

The answer, to be discussed in this article, is the usual answer in welfare economics: ‘It depends.’ Depending both on the source of the distortion and the parameters of buyer preferences , corrective insurance may sometimes be strongly demanded, might or might not be expected to occur, or be unlikely to happen in unregulated insurance markets.

For example, the idea that individuals can be incentivized to change behaviors that are harmful to them is at the core of the normative appeal of behavioral economics (Della Vigna and Malmendier, 2006). Beginning with the observation that people with given incomes faced with a set of prices for different goods and services sometimes make mistakes, and sometimes do so in predictable ways, economists have developed normative analyses to show how incentives including prices can be changed to nudge, push, or drive people away from these consistently irrational acts into behaviors that will end up making them better off, at least in some way and along some dimensions (Thaler and Sunstein, 2008; Kahneman, 2011).

Both healthcare and health insurance have, not surprisingly, been prime candidates for nudging. Because information about illness and medical treatment is imperfect (for consumers, but also for providers of care and suppliers of insurance), there are many cases in which choices are made that turn out to be wrong later. More relevantly, there is also suspicion that consumers have less information than the maximum amount available, and so may make choices that do not maximize expected net benefit, either for them or for society. As a result, there is interest in changing how health insurance is designed and sold in order to improve matters (Chernew et al., 2007; Fendrick and Chernew, 2009; Fendrick et al., 2012). The most prominent (but not the only) example: if consumers do not have a full evidence-based understanding of the benefit from some treatment, and systematically use less or more than the amount that would maximize expected net benefit, might cost sharing for that treatment be changed in ways that help (Pauly and Blavin, 2008)?

In much of the analysis, the identity of the agent who is going to be doing this incentive changing is not specified; it is enough to show that ‘we’ could change things in such a way as to make ‘us’ better off. In some of the specific applications to such things as employee retirement benefits (Madrian and Shea, 2001), the implicit incentive-planner would plausibly seem to be the employer, though the proof that doing things that make workers better off will also make the stockholders of the firm better off is usually absent. In the largest share of this literature, it is government, broadly imagined as an entity interested in maximizing ex post economic welfare, that appears to be the intended customer for the normative advice (Bernheim and Rangel, 2009). What is probably least common is a serious investigation of the question whether or when voluntary markets in behavioral change might emerge and function efficiently.

This article investigates under what circumstances consumers might choose to change the health insurance incentives they face in order to bring about behavior which is likely to make them better off. (What exactly ‘better off’ means will be important.) Although attention will be paid to the risk reduction benefits of insurance, it is also worth noting that the main tradeoff in insurance – pay a higher fixed amount initially (the premium) in order to reduce the price at point of use later (the coinsurance) – is the same structure that has been studied for health clubs, great book clubs, and other examples of devices to bring about behavioral change.

In this model consumers can be perceptive about their failings; they are assumed to be able to understand that sometimes, for various reasons, they may not choose behavior which is ex post optimal for them, or that something needs to be done, either to information stock or user prices, to improve choices. Therefore, it is necessary to investigate whether it is possible that insurance that covers its costs and corrects such failings that will be demanded. It is assumed that supply is competitive so insurers will supply the kind of changes consumers might demand.

A main finding is the likelihood that consumers will voluntarily agree to be nudged depends critically on the reason why their behavior was nonoptimal in the first place, and even then, on the values of key variables in the problem. Sometimes there will be demand for nudging, and sometimes not.

Outlined here is a simple model of economically efficient cost sharing when consumers might underestimate the marginal benefit of some kinds of medical care; also indicated here is the voluntary insurance and medical care choices these consumers would make in such a situation, compared to what they would choose if they correctly estimated benefit. Then it is asked whether and when consumers would be willing to choose something different from this choice of both insurance and medical care, is there something else that they would prefer and which would make them better off? One fairly tautological model is provided where the outcome of voluntary efficiency-increasing nudging does occur with competitive insurers. That model is compared as a benchmark with other stories that raise serious issues of whether people will voluntarily demand the incentive-changing mechanisms that will make them better off, and whether insurers will supply them if they are demanded. It is shown that under not implausible assumptions there are some cases in which voluntary demand will not materialize in the ideal way, and it is explained why. At the end the question addressed is whether institutional arrangements alternative to voluntary insurance markets, like public sector interventions, can do better, and show that government in a democratic setting might be subject to similar problems.

The Core Model

The model is one of competitive insurers choosing to offer policies with possibly different levels of cost sharing for different services. Two kinds of services, ‘preventive’ and ‘treatment,’ come to mind. The distinction is that a ‘preventive’ service affects the probability of future health or illness states, whereas a treatment service provides only short-term (if valuable) benefit when an illness strikes. Thus a preventive service both provides benefit in the form of improved future health and potentially lower demand for treatment if illness is avoided; the concept includes both what is usually labeled prevention but also the great majority of other health services in the first stage or early onset of some illness that affects what happens to health later.

In the absence of insurance, demand for either kind of service bought in a competitive market by fully informed consumers would be (presumably) first best optimal, at the point where marginal benefit equals marginal cost. For treatments of this condition, this just equates the (money) value of current period health benefits to price, assumed to be equal to marginal cost. For preventive services, both current period cost and future ‘cost offsets’ are part of the full marginal cost, whereas the value of expected future health (if care were costless) is the measure of marginal benefit. Alternatively, the value of marginal future health could be combined with cost offsets as a measure of benefit, to be equated to the current period price or cost of preventive care.

A simple version of the first order condition for optimal preventive care use would be:

where ∆П is the change in probability of future illness due to consumption of one more unit of the preventive service, DUH is the marginal utility of future health (comparing health in the illness state vs. health in the healthy state), l is the marginal utility of money, and C is the cost of treating the future illness.

If there is no insurance coverage, consumption of both services will be at the optimal level. In particular, the consumer in deciding on consumption of the preventive service will take future reductions (cost offsets) for the cost of treatment into account, along with the value of health benefits. That is, the consumer sees and satisfies condition, eqn [1]. However, if there already exists coverage of the treatment, and there is a positive cost offset, there should be insurance coverage of the preventive service that reflects the part of any cost offset for treatment that is covered by insurance. This is a second-best argument. In the absence of such an adjustment, the consumer ignores the cost offset term, and under consumes the preventive service.

In the limiting case in which the expected cost offset (DPC) exceeds the price of the preventive service, and the other service is fully covered, insurance coverage of the preventive service should be 100% in the absence of insurance administrative and claims processing costs, regardless of the degree of price responsiveness (Glaser and McGuire, 2012). If there is a positive marginal administrative cost to insurance coverage, that consideration would reduce the ideal extent of coverage. If there would be positive use of preventive care in the absence of coverage, then coverage should be higher the greater the price responsiveness of the use of coverage to cost sharing (Held and Pauly, 1990). If price responsiveness is low, coverage per se may increase the aggregate expected insured expenses, and the higher premium is offset by these higher benefits. However, if there are administrative costs, those additional costs, when applied to paying benefits where use would have occurred in any case, are wasteful.

The Setting And The Behavioral Model

This simple case is well known. But the more interesting questions arise in one of the most frequently discussed (and topical) applications of behavioral economics: the idea that cost sharing in health insurance might be used to guide people to choose more efficient levels of consumption of effective medical care than they might otherwise select, which is commonly called ‘value-based’ cost sharing in the health insurance literature (Chernew et al., 2007). The alternative model in the discussion is usually one in which cost sharing is uniform across all settings associated with a given level of spending (e.g. 20% coinsurance or a $1000 deductible for all covered medical expenses); it is alleged that value-based cost sharing will produce a better outcome than this.

But this status quo is not the best alternative system. The theory of optimal insurance (Pauly, 1968; Zeckhauser, 1970) envisions varying coinsurance as well, but for different reasons and in different ways than prescribed by value-based cost sharing. Therefore, the question arises whether value-based cost sharing that dominates some or all of these alternatives in terms of ex post net benefits would be preferred by consumers.

The benchmark framework in mind is this: competitive insurers in unsubsidized and unregulated markets are free to set cost sharing levels (as proportional coinsurance) at different levels for different services. Consumers choose among insurance plans based on their premiums and their cost sharing. Each insurance plan’s premium must cover the costs of the benefits it pays out plus administrative expenses, and may yield positive economic profits if the market is not competitive. The first question is whether a plan that selects the level of cost sharing prescribed by the value-based approach will be preferred by consumers to plans offering other levels of benefits and associated premia. (The second question, whether insurers will offer that plan, will be considered later in the article.)

It has been shown (Pauly and Blavin, 2008) that, in the absence of cost offsets, a necessary condition for value-based cost sharing to improve outcomes in competitive insurance markets is that the patient’s marginal benefit or demand curve differs from the curve that represents true marginal benefits. If patients always consider correctly the value of effective medical care, they will use highly (marginally) effective care even if cost sharing is high, but will use only less marginally effective and inefficient care if cost sharing is low. To control this moral hazard, coinsurance will be chosen to make the second-best optimal tradeoff between such overuse and risk protection. Moreover, under full information but with variation across types of care in patient response to cost sharing, uniform cost sharing will not be optimal; rather, other things equal, optimal cost sharing will vary directly with patient demand responsiveness. No further consideration of ‘value’ is needed to specify the ideal level of cost sharing.

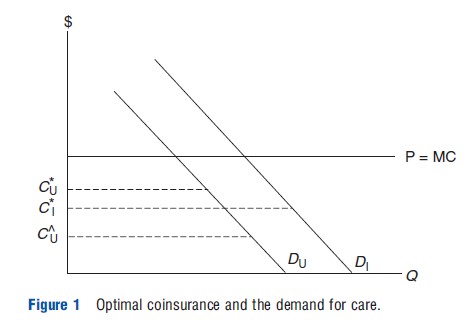

Figure 1 provides an illustration of this model. DI represents the true marginal (expected) health benefit curve for some kind of care; MC is its cost and price net of cost offsets. (This service is both uncertain and has a positive marginal net cost; cost offsets from its use are not sufficiently large that consuming more of it reduces total benefits cost.) Because of uncertainty, it is assumed that consumers get benefit from insurance coverage of this service. There is a (second best) optimal level of coinsurance, indicated in the diagram as c*1, which consumers will also prefer to any other level of coinsurance. At this point the marginal welfare cost from lowering coinsurance will equal the marginal benefit from further risk reduction. At that point, the quantity will be second best optimal. Optimal coinsurance (other things, including risk characteristics and risk aversion, held constant) will be lower for less price responsive types of care and higher for more price responsive types of care. In all cases, the marginal benefit will be less than the marginal cost. At this optimal pattern of coinsurance, the value or marginal benefit from each type of care will equal the level of coinsurance per unit. At a given level of coinsurance, when informed consumers are in equilibrium, no one type of care will have higher marginal value than any other, so there is no need to further vary coinsurance with value. However, at the optimal level of coinsurance the marginal value of less price responsive care will be lower than that for more price responsive care because the lower coinsurance that leads to a lower value provides an offsetting benefit in terms of better risk protection.

Deviations From Optimality

Now suppose that the marginal benefit curves that patients are using are lower than the true curve. What then? Start with a simple comparison. Suppose that three plans are offered. One (informed plan) sets the coinsurance rate (as described above) at the optimal level given the consumer’s risk aversion and given the marginal benefit curve that would be generated if patient demands were based on accurate estimates of the marginal benefit from different amounts of care. However, patients are assumed to underestimate the benefit from some important service, and so would consume less than the full optimal information amount if they were in the first plan. The inaccurate expected marginal benefit curve is indicated in Figure 1 as DU. So an alternative value-based plan (Nudge Plan) is offered with lower cost sharing at cU. The purpose of the lower cost sharing is to offset the effect of benefit underestimation by increasing quantity demanded by using a lower user price. This is the optimal level of cost sharing, given that the marginal benefit curve is underestimated.

There is, however, a third alternative insurance plan, one that the consumer might prefer: Specify c*U, the coinsurance rate and premium that would be optimal given the actual (though underestimated) demand, and the lower rate of use and lower premium associated with that plan. The uninformed plan generally has a higher coinsurance rate (at c*U) than either cU or c*1, with both a lower premium and lower expected medical costs than the Value-Based Nudge Plan. The reason why the coinsurance rate is generally higher than with the true marginal benefit curve is that, with lower demand at any level of coinsurance, there is less risk.

Figure 1 depicts each of the three plans under alternative assumptions that the marginal benefit curve is the informationally correct demand curve DI or the actual (uninformed) demand curve DU. Note that the welfare cost of moral hazard is smaller at all coinsurance levels along the DU curve than it would be under the informed plan with the informed demand curve.

The Gain From ‘Nudging’

This simple example shows that there can be gains from getting the consumer to choose the Nudge Plan. How does the size of the gain vary with the position of the uninformed demand curve? The answer depends in part on whether the informed plan or the uninformed plan is used as a benchmark. The case is simplest if welfare under the Nudge Plan is compared with what it would have been under the fully informed plan. Pauly and Blavin (2008) show that, over some of the range of possibly underestimated demand curves, welfare may actually be higher with underestimation and the Nudge Plan than with the informed plan. This is what they call the ‘benefit of blissful ignorance.’

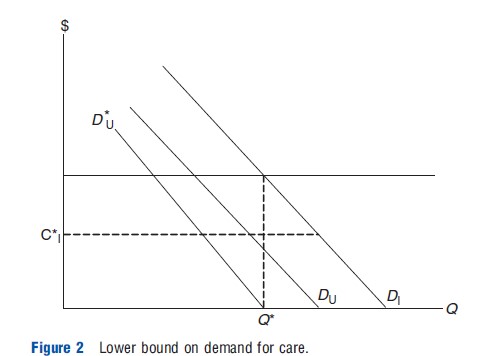

There is obviously a gain from permitting the marginal benefit curve to fall short of the true curve as long as it remains above that curve which hits the x-axis at the optimal level of use (ignoring income effects). That curve is D*U in Figure 2; should it prevail, coinsurance can be set at zero and yet use will be first best optimal (ignoring income effects). The consumer can completely avoid the consequences of moral hazard, and have both full protection against risk and optimal use of medical care. To the left of D*U welfare begins to fall, but remains above that with the informed plan at c*1 some range.

Modeling Deviation

With this as background, a model can be made of the causes of deviations in the patient’s marginal benefit curve from the true value and corrective strategies. Begin by thinking of what kind of medical service would be one for which consumers would demand insurance but underestimate true marginal value. Think of a service for which demand is stochastic today and which affects health tomorrow. Although some acute-care services yield immediate utility benefits (analgesics, suture of a bleeding wound), the bulk of medical services are of this ‘two-period’ character. Statins for people who have already had a heart attack, asthma medications, and cancer surgery are all things that a person might or might not need, depending on the onset of the chronic condition, but which then all generate disutility in one period in return for a benefit in the future. (There are some complexities associated with insurance coverage over multiple periods which will be ignored for the present.) The person decides on insurance coverage for such services at time t0. It is assumed that there is such a service with a (gross) market price in period t of Pt and nonmarket costs (time, pain, bother) of C, all incurred at time t1. If the person consumes the service, health is increased in period t + 1 and future periods.

The first order condition for optimal choice (slightly rewritten) is:

Here ∆Ct+j is the cost offset in the J(j = 1,2,y,J) future periods the person will pay, MHt is the value of the additional health at time t from the service measured in dollars, and r is the interest rate; the expression on the right gives the present discounted dollar value of additional health. It can be assumed that MH falls as the service is consumed at a higher rate. That is, the consumer compares the price with the discounted marginal benefits minus any nonmonetary cost from treatment.

There is only one way a consumer can estimate marginal benefit correctly, but there are (apparently) many incorrect ways to do it. Consider patient non-adherence to a physician’s prescription to use some product or service, conditional on a diagnosis of some chronic condition. The things that can be, apparently, estimated or considered incorrectly are all in eqn [2]: the cost offset (because of insurance coverage), the value of the marginal health product or the service, the interest rate, and the nonmonetary cost of the service.

Insurance coverage distorting the consumer’s value of the cost offset is one reason why patients may not use the care they should. Imperfect information is another likely reason offered, especially if patients have difficulty understanding the physician’s explanation for some prescribed treatment. In addition, if people use nonexponential discounting, they may fail to consume services of high marginal (future) benefit, even if they correctly perceive that benefit, because they underestimate the value of that benefit. Quasi-hyperbolic discounting would be one way to model this imperfect discounting. Finally, the nonmonetary cost itself may be high, higher than is perceived by the physician who recommends the service and is then disappointed when patients are nonadherent to the recommendation. In this case it is the information for the potential ‘nudger’ that is incorrect, but it is a possible scenario for trying to persuade consumers to change.

The case for voluntary value-based cost sharing as a function of these four rationales for value-based cost sharing will now be explored.

The Best Case For Voluntary Value-Based Cost Sharing: Positive Insured Cost Offsets

The most obvious case why some level of coinsurance might be too high is if there are positive cost offsets (the current preventive service reduces future costs along with improved health) and, although those future services are covered by insurance, that is not taken into account in specifying the coinsurance for the preventive service. Then in calculating marginal benefit the consumer fails to take these reductions in cost (and in insurance payments to cover those costs) into account.

Most of the examples of the success of value-based cost sharing deal with this case. However, the conventional theory of optimal voluntary coinsurance in competitive markets is already supposed to have taken these effects into account because the cost of the preventive service is the net (of cost offsets, positive or negative). The idea is that the insurer will recognize these effects, and build them into the premium adjustment that matches any change in the level of coinsurance for the service. This happy state of affairs can be impeded if there is turnover among insureds – if the person potentially leaves the plan before the cost offsets occur. Other than this, however, the market solution to this case is well known; it is one in which the consumer does not require extra nudging beyond what would have been built into optimal insurance in the first place. The consumer notices that the plan with ‘nudging’ coinsurance carries lower premiums and better benefits than any other, and chooses that plan.

A Good Case For Voluntary Value-Based Cost Sharing: The Consumer Looking To The Future Seeks To Control His Irrational Current Self

The strongest behaviorally motivated case for the value-based plan is to note that it is the plan that maximizes ex post utility, given the underestimated demand curve and the true marginal benefit curve. It is the former curve which describes behavior, but the latter which describes the actual outcome and its value. A split-personality or self-control model is a very common approach in the literature to this case, usually applied in cases where discounting is hyperbolic or inconsistent in some way. The approach of Della Vigna and Malmendier (2006) and Della Vigna (2009) that they used for health club annual memberships (as opposed to paying per use of the gym), modified to fit the health insurance case, will be followed.

The idea is the consumers realize that, although they should exercise, get their test, or take their medicine, because of lack of self-control they will not do so when they are facing the full price per unit, or even at the full information ideal level of cost sharing. They therefore prefer incentives that will be set at a level such that, given their expected attenuated future demand behavior, they do what they should. They therefore sheepishly prefer a plan with low enough cost sharing to get them to do what they ought to with any alternative, because it dominates all other alternatives in terms of ex post net benefit. In this case, the most common interpretation is that it is not that the consumer misperceives, it is that he or she misbehaves.

An alternative interpretation, based on the psychological work of Zauberman et al. (2009) is the consumer misperceives time. Exponential discounting of misperceived time can be equivalent to hyperbolic discounting of correctly perceived time. Either way, this case can be described as resulting from using a discount function that differs from the conventional exponential one – for example, by being hyperbolic.

Formally, imagine multiplying the discount rate (1/(1 + r)) by a term B that reflects the underestimation of the value of future benefits (at time t + 1 and later). This value is the one the consumers attach to future benefits at the time t when they might consume the costly and bothersome service. The usual model at this point imagines that the consumer considering precommitment at time t0 with regard to behavior at time t1 seeks to reproduce the behavior at time t1 which would have occurred under exponential (nonmyopic) discounting (Rasmusen, 2008).

But in this case the paradoxical results on optimal underestimation means that the goal is not to get the consumer to fully correct the imperfect discounting. Doing that would lead to the DI demand curve, although utility is higher if the demand curve is only at D*U. Put slightly differently, in deciding how to control one’s ‘bad’ self in the two-selves model, one does not want to get that second self to do what the first self would have done under a fully correct perception of the discount rate. Instead, one wants to adjust cost sharing to produce a rate of use potentially greater than current (myopic) self-use and coverage but not as much as would be used by the nonmyopic self. In effect, the first self takes advantage of the impatience of the second self as a way of controlling moral hazard on services with preventive benefits. Far from wanting to correct a later shortsighted behavior, one would want it to remain shortsighted, just not as much.

There is an additional issue here of some potential importance. It may well be that the decision to precommit in period p0 changes the person’s demand curve in period p1 when period p1 arrives. That is, recognizing the arrangements for precommitment, the person may be less resistant to proper discounting; there may be feedback from the decision to precommit to behavior in some event to the behavior that would occur in that event. This might be especially likely to happen if Zauberman’s model of discounting holds: observing the precommitment device changes how one thinks about time closer to its true value. If this happens – if the discounted marginal benefit curve in period p1 is moved closer to the true curve (as perceived in period p0, or period p2 or later), then the structure of the precommitment device – the lower user price – will need to be changed to one that has a higher user price. But if the demand curve is shifted up enough, the expected utility under precommitment may actually end up lower than at the initial no-precommitment point. In this case no voluntary nudging will occur.

More generally, what is the ideal level of cost sharing in such self-control cases? It depends on the position of the uninformed marginal benefit curve relative to the true curve. At one extreme, if the reduction in demand is so great that the quantity demanded at a zero user price (full coverage) is less than or equal to the quantity at which true marginal benefit equals marginal cost, then optimal cost sharing is zero regardless of risk or risk aversion. (Negative prices are ruled out in favor of the corner solution.) If the quantity at a user price of zero is greater than the quantity at which marginal benefit equals marginal cost, then the optimal extent of coinsurance is calculated, as in Pauly and Blavin, (2008), by comparing the true marginal welfare cost with the marginal risk premium given the level of use and loss distribution that prevails under the underestimated demand curve, taking into account the person’s risk aversion or ‘risk premium.’ It will be optimal to have some positive coinsurance for the person who lacks selfcontrol as long as the distortion is not too large. (This question will be regarded when the alternative form of nudging is considered involving providing information on what the marginal benefit actually is.)

The consumers will voluntarily choose the cost sharing option that precommits them to lower payment per unit in return for payment of a lump sum payment (premium or membership). This provides two kinds of gain. To the extent that the use of the service is stochastic (Della Vigna (2009) describes even health club visits as stochastic), there is a risk premium gain to a risk averse person from paying some of the expected cost in advance. And then there is the gain in expected utility from precommitment.

How binding is the precommitment? Once the people are facing the possibility of paying for and using the preventive service, they attach less value to using it and, in view of low likely use, would prefer an insurance with higher cost sharing and lower premiums. There is no absolute barrier to changing insurance coverage at any point in time; usually contracts for employment related coverage are for a year but individual insurance can be changed at any time. However, it is likely that no single specific coverage would motivate a change – our consumer in the throes of myopia would just prefer insurance with less coverage of preventive care in general. One could model the decision to renege as based on a comparison of the transactions costs of changing behavior versus the difference in expected utility between the precommitted coverage and the myopically optimal coverage. Of course, if the medical event occurred close to the time when the person is deciding to make an annual election, things could be different.

Better Information As The Solution

Another reason for benefit underestimation is imperfect information about benefit. One strategy is to provide information. But when would it be socially efficient to provide information? If marginal benefit is underestimated by a sufficiently large amount, more information may help; if not, more information may do harm, even if it is costless, as discussed earlier.

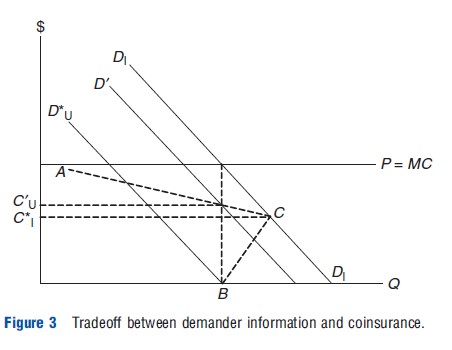

Imagine varying the DU curve by changing information, and plot various levels of coinsurance.

As illustrated in Figure 3, if the nudger can control both information and the coinsurance rate, it would provide no corrective information but set coinsurance along the BC line. In contrast, if it can only control information but consumers choose coinsurance along AC, it would choose information to move the marginal benefit curve to D`, where use at the consumer-chosen coinsurance rate C`U is just at the optimal level.

But in the context of voluntary choice of insurance, it may be hard to be explicit about keeping people ignorant. Thus both characterization of settings in which leaving underestimation untouched is a good strategy and asking whether people will voluntarily and explicitly choose to leave things that way, is required.

Here is the source of a serious dilemma. The simplest explanation is to assume that the consumer focuses only on the final outcome (in terms of comparison of health improvement, premiums, and expected out of pocket costs), recognizes that this outcome is superior to that with the uninformed plan, and therefore prefers the nudge plan with a health outcome which (given its cost) is better ex post. The dilemma arises if the consumers reflect on the source of this improvement. Suppose they realize that it comes from the fact that the initial perceived marginal benefit curve was incorrect, and was less than the true curve. But if the consumers become aware of this fact and respond by increasing their demand curve, use and outcomes under the Nudge plan’s coinsurance rate will not replicate what is anticipated under the informed plan. Instead, faced with a relatively low coinsurance rate, use will be higher. Health outcomes will be even better than under the informed plan, but (in the short run) the insurer will lose money, and, after seeing an increased premium to cover this higher use, the consumer will judge the higher premium and higher expected out of pocket cost to overshadow the health improvement. If the demand curve shifts all the way to the true demand curve, the ideal coinsurance rate will also rise to the level that is optimal.

For information to work properly to achieve a better outcome, the consumer must purchase insurance and care based on the uninformed demand curve. But to be motivated to buy the plan, the consumers may need to know (and be convinced) that the health outcome they will achieve at the level of use they target under the plan’s coinsurance rate will be much higher than they would expect. This is the heart of the dilemma: they will prefer the nudge plan only if they think their health outcome will be better than what they think it will be as embodied in their (uninformed) demand curve. Convincing them of this will arguably shift the actual demand curve.

Putting the pieces together, it is noted that the strategy of improving information only improves ex post welfare if the marginal benefit curve is below D*U. Even then, the uninformed demander will not be willing to pay the higher premium for better coverage as long as they remain ignorant. Providing information can shift the demand curve for care and coverage, so if information is relatively cheap and effective it may pay for a firm to charge a little more after paying to shift demand. Even here, however, the level of coverage will be on the AC-locus, not on the BC-locus. Merely offering the optimal level of coverage on any underestimated demand curve will not be persuasive. To get the consumers to prefer coverage on the BC-locus one would have to fully inform them, but then demand would shift to a level with higher coinsurance and higher moral hazard. Less information means less moral hazard but less correction in coverage. It does not seem possible to reach the first best outcome in a voluntary way.

The Cost Of Bother

Both imperfect self-control and imperfect information are reasons why demand does not reflect marginal health benefit. But the informal literature on adherence also suggests another reason: The consumer forgets, or it is too much bother – there are subjective costs. In effect, there are additional costs on top of any cost sharing. It is these subjective costs that shift the marginal benefit curve downward.

But note that what prompts them to take their medicine is the lower user price, implying that decisions are made rationally by comparing perceived benefits to ‘short run’ costs including time and bother. In the ignorant case it is the perceived benefit estimate that is wrong; in the ‘bother’ case there are some additional (uninsured) costs. If these costs are expected to be real (that is, if people know from past experience that they must work hard to remember, and do not just overestimate the actual effort in remembering), then people will expect to incur those costs if the user price is lowered enough to result in the desired behavior. Here again, but for a different reason, ex post welfare will be lower under the Value-Based Nudge Plan, and people may refuse to be subject to the push.

Perception Of Nonmonetary Cost

Another reason why people may fail to follow provider advice about services which affect future health is because they experience or expect to experience nonmonetary costs associated with those services. Those costs may represent physical side effects (nausea, impotence, dizziness) or they may represent the effort needed to remember to take the medicines or treatment on the prescribed basis or even the bother of filling the prescription.

In the first best world these costs will be taken into account in determining the net marginal benefits, but in the setting in which physicians write prescriptions they may have a difficult time knowing what these costs are. If they prescribe based on, say, the average patient’s net benefit from a drug, those who have above-average nonmonetary costs may rationally choose not to comply; there may be rational nonadherence. Lower the user price, and there will be more adherence as those who rationally failed to adhere when they were exposed to the full monetary cost of the treatment and their nonmonetary costs now find positive net benefit when the nonmonetary cost falls. But when confronted with a higher premium to pay for this change in future behavior, this group will correctly judge its net benefit to be negative.

Other Threats: Heterogeneity

What will the market look like if some consumers underestimate marginal benefits but others do not? If some consumers understand marginal benefits correctly but insurers cannot tell who is who, the well informed patients will find it advantageous to themselves to be pooled with other underestimating consumers who use less care at given coinsurance levels. The breakeven premiums will then reflect an average of the use of both classes of consumers, just as in conventional adverse selection models, which will make low coinsurance value-based policies even less attractive.

The Mixed Case

Now consider the most complex but probably the most realistic case: one in which patients underestimate the true marginal benefit curve (imperfect information) but also overdiscount those benefits (imperfect discounting). If the underestimation can be kept secret, the consumer might be willing to agree to a plan that lowers the user price enough to offset the imperfect discounting.

The key issue here as before is how far the demand curve is shifted to the left by these two influences. If it is still to the right of D*U, the two-self model will tolerate some reduction in cost sharing without having to turn to information to move the curve. The change will be the utility maximizing coverage based on a correctly discounted but underestimated marginal benefit curve.

Focus Group Evidence

A series of focus groups using subjects from the state of Michigan were asked about various aspects of alteration of insurance coverage to vary cost sharing with measures of clinical (net) value using a set of scenarios (Swinburn et al., 2012). There was no scenario based on quantitative values for changes in use of care, health outcome, and total medical spending or premiums but there are some qualitative results of interest for the models that have been discussed.

One scenario proposed lowering copayments to zero for a medical condition (diabetes) thought to be characterized by underuse of recommended care and poor health outcomes. The scenario envisioned cost offsets in employment based insurance (patients with lower cost barriers are more likely to stick with the care they need, which would make them ‘more likely to use fewer healthcare dollars’), but the total premium will initially increase though the employer ‘expects to make it up with healthier employees’ and will eventually have less costly health insurance.

Participants generally supported the intervention as described but with several caveats that are important for our analysis. First, they would support lowering copayments for diabetics ‘only if the program saved money.’ Although this response is somewhat vague, a reasonable interpretation is that they would not favor the program if premium costs they had to pay were increased even if health was improved for those workers with diabetes. There was also an equity consideration that offset efficiency gains: discounts should be available (a majority thought) only to those low income people who could not afford the prior cost sharing – even if lower cost sharing might change behavior of wealthier participants in a health-improving way.

The other interesting finding was also couched in terms of equity. It was felt to be unfair to provide lower cost sharing benefits to people with conditions under which they failed to follow physician advice. This was both rewarding irresponsible behavior and failing to reward people with conditions where adherence was high, or who had no chronic conditions. These observations could also be interpreted as referring to risk selection, benefitting high risk patients who behave incorrectly at the expense of those who manage their care properly or are low risk to begin with.

Overall, respondents felt that this new design should be used some of the time, but only in certain circumstances.

Another report (Midwest Business Group on Health and Buck Consultants, 2012) obtained similar results from another set of focus group participants. There was skepticism about the ability of insurers to identify these cases, and a feeling that those who were compliant needed the help of lower cost sharing more than those who were less compliant.

Solutions

Solutions to these problems depend in large part on the cause. In the case of people with understanding of self-control problems, there should be a demand for nudging even without any intervention. Here providing accurate and persuasive information on the actual benefit ex post will be helpful not only to get the demand as right as it can be but also to motivate the demand for insurance.

For people who underestimate marginal benefit because of information imperfections, the strategy of providing information on actual benefit may backfire, as noted, because it will be associated with a greater rate of use in inefficient situations. There is a partial solution that may work in some cases. Suppose that the perceived marginal benefit curve is to the left of D0 . Then it is possible that the utility under full information with cost sharing at the optimal level is higher than the utility with no action. In such a case providing information about the true curve and then doing the best that can be done may be preferred to the original state.

However, in this case the optimal and demander-chosen levels of coinsurance coincide; there is no need for value-based adjustments. In the more general case, it seems difficult to get the person to prefer the insurance with value-based cost sharing a priori.

Bibliography:

- Bernheim, B. D. and Rangel, A. (2009). Beyond revealed preferences : Choicetheoretic foundations for behavioral welfare economics. Quarterly Journal of Economics 124, 51–104.

- Chernew, M. E., Rosen, A. B. and Fendrick, A. M. (2007). Value-based insurance design. Health Affairs 26, w195–w203.

- Della Vigna, S. (2009). Psychology and economics: Evidence from the field. Journal of Economic Literature 47, 315–372.

- Della Vigna, S. and Malmendier, U. (2006). Paying not to go to the gym. American Economic Review 96, 694–719.

- Fendrick, A. M. and Chernew, M. E. (2009). Value based insurance design: Maintaining a focus on health in an era of cost containment. American Journal of Managed Care 15, 338–343.

- Fendrick, A. M., Martin, J. J. and Weiss, A. E. (2012). Value-based insurance design: More health at any price. Health Services Research 47, 404–413.

- Glaser, J. and McGuire, T. G. (2012). A welfare measure of ‘offset effects’ in health insurance. Journal of Public Economics 96, 520–523.

- Held, P. J. and Pauly, M. V. (1990). Benign moral hazard and the cost-effectiveness analysis of insurance coverage. Journal of Health Economics 9, 447–461.

- Kahneman, D. (2011). Thinking, fast and slow. New York, NY: Farrar, Straus, and Giroux.

- Madrian, B. C. and Shea, D. F. (2001). The power of suggestion: Inertia in 401(k) participation and savings behavior. Quarterly Journal of Economics 116, 1149–1187.

- Midwest Business Group on Health and Buck Consultants (2012). Communicating value-based benefits: Employee research project results. Center for Value-Based Insurance Design, University of Michigan.

- Pauly, M. V. (1968). The economics of moral hazard. American Economic Review 58, 531–537.

- Pauly, M. V. and Blavin, F. E. (2008). Moral hazard in insurance, value-based cost sharing, and the benefits of blissful ignorance. Journal of Health Economics 27, 1407–1417.

- Rasmusen, E. B. (2008). Some common confusions about hyperbolic discounting. Working Paper No. 2008–11. Bloomington, IN: Kelley School of Business, Department of Business Economics and Public Policy, Indiana University.

- Swinburn, T., Ginsburg, M., Benzik, M. E. and Clark, R. (2012). Probing the public’s view on V-BID. Ann Arbor, MI: Center for Value-Based Insurance Design, University of Michigan.

- Thaler, R. H. and Sunstein, C. R. (2008). Nudge: Improving decisions about health, wealth, and happiness. New Haven, CT: Yale University Press.

- Zauberman, G., Kim, B. K., Malkoc, S. A. and Bettman, J. R. (2009). Discounting time and time discounting: Subjective time perception and intertemporal preferences . Journal of Marketing Research 46, 543–556.

- Zeckhauser, R. J. (1970). Medical insurance: A case study of the tradeoff between risk spreading and appropriate incentives. Journal of Economic Theory 2, 10–26.